1. The most difficult part of managing other people’s money

The responsibility of having other people’s money really weighed on me. If you have a 10-year time horizon, you can make good decisions and make a lot of money. If you have a three-year time horizon, you could probably still do well. But if you have only a three-month time horizon, anything can happen.

2. Claugus uses Bollinger Bands (2 standard deviations) on S&P 500, the Nasdaq 100 and Russell 2000 to define his market exposure to indexes.

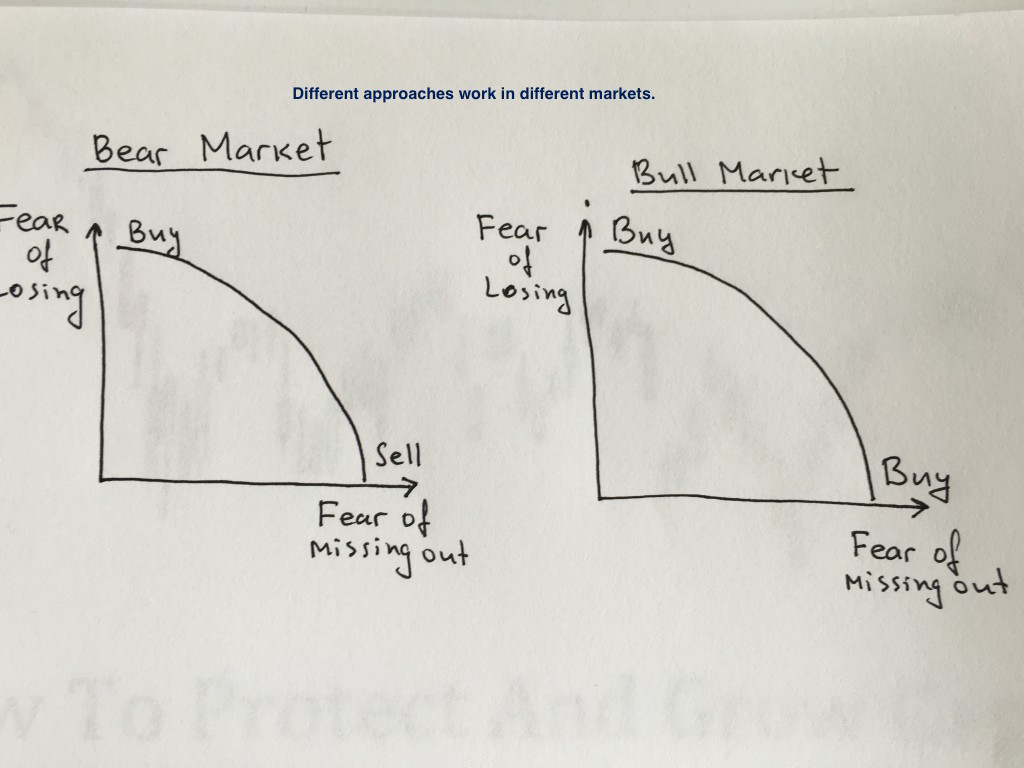

I am a reversion-to-the-mean thinker. We use standard deviation bands to define extreme readings.

At the lower band, we would be 130 percent long and 20 percent short. At the midpoint, we would be 100 percent long and 50 percent short. We are 50 percent net long at the midpoint rather than neutral because of the long-term secular uptrend in stock prices. At the upper band, we would be 90 percent short and 20 percent long, or 70 percent net short. Our net exposure will increase as the market goes down and decrease as the market goes up.

After determining the portfolio net exposure, we do a similar analysis by sector, trying to identify sectors that are cheap and sectors that are expensive.

3. Incentives matter. For many money managers, career risk trumps market risk. As the saying goes – it is better to fail conventionally than to succeed unconventionally.

During the fourth quarter of 1999, when the market was skyrocketing and I was net short, I was losing my ass at the same time most other hedge funds were making a ton of money. When your investors look around, and you’re losing money, while everyone else is making money, they are much more likely to pull their investment. Being short in a rising market is very difficult from an investor relations standpoint. In 2008, we were losing money, but so was everyone else. It’s a lot easier to keep your capital base in that type of scenario.

4. Bull markets are low-correlation markets of stocks. Bear markets are high-correlation stock markets.

When the market sells off really hard, as happened in late 2008 to early 2009, it is usually a matter of liquidity. There’s no place to hide in a liquidity sell-off; people sell everything because they have to, not because they want to. The reverse rarely happens on the upside. People don’t run out and buy everything. There are always some stocks that are going down. The interesting thing is that shorts are actually easier to find than longs. It is easier to spot a broken company than a good company. It is easier to identify bad management than good management.

5. The market is forward-looking and myopic at the same time. It does not look too far into the future because the further in time, the higher the uncertainty of cash flows. Some managers take advantage of this short-term nature of the market by being proactive and looking further than the market could see. The single most important concept in his stock selection process – look for future revenue generation that can be reasonably anticipated but that is not reflected by the current market price.

I often find that the market won’t pay anything for production potential that is more than a year away.

I look for anomalies. When I screen quarterly earnings, I look for quarterly earnings that are up more than 50 percent or down more than 30 percent.

One of Claugus’s major themes in selecting individual stocks is looking for companies that will benefit from a future development that is not being priced into the current market. The source of the improvement can take many forms including anticipated new sources of production, new technology, an expected increase in asset values, and so on. Claugus says that if a revenue source is more than a year away, the market will often fail to assign any significant value to it.

Sometimes, you will take a look at a momentum stock that is trading at a P/E of 50 and you will quickly dismiss it as richly valued. P/E reflects market expectations and a P/E of 50 is way too high. Well, if this stock continues to double revenue and triple earnings, trading at P/E of 50 could actually be cheap – a bargain. Context is really important.

Source: Schwager, Jack D. (2012-04-25). Hedge Fund Market Wizards. John Wiley and Sons.

Don’t forget to check out my newest book: Top 10 Trading Setups – How to find them, when to trade them, how to make money with them.