This week, Google marked 10 years since it became a public company. Here’s a quick reminder of the event from wikipedia:

In October 2003, while discussing a possible initial public offering of shares (IPO), Microsoft approached the company about a possible partnership or merger. The deal never materialized. In January 2004, Google announced the hiring of Morgan Stanley and Goldman Sachs Group to arrange an IPO. The IPO was projected to raise as much as $4 billion.

Google’s initial public offering took place on August 19, 2004. A total of 19,605,052 shares were offered at a price of $85 per share. Of that, 14,142,135 (another mathematical reference as √2 ≈ 1.4142135) were floated by Google and 5,462,917 by selling stockholders. The sale raised US$1.67 billion, and gave Google a market capitalization of more than $23 billion. Many of Google’s employees became instant paper millionaires. Yahoo!, a competitor of Google, also benefited from the IPO because it owns 2.7 million shares of Google.

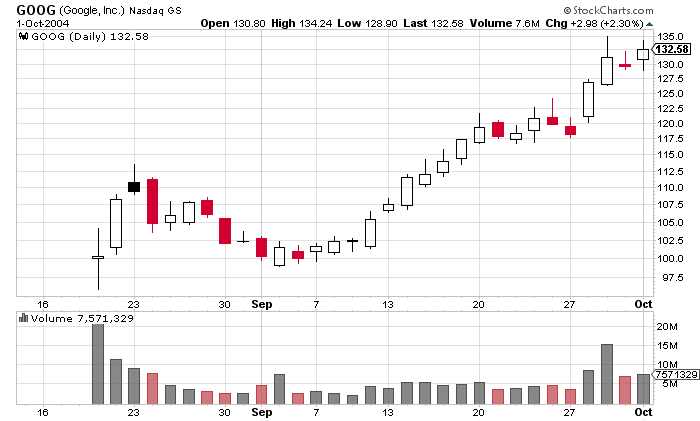

For those that don’t remember how $GOOG traded, here’s a chart of the first couple months after its IPO.

10 years ago, Google was trading near $100 with a P/E of 130. Today, it is trading near $600 with a P/E of around 30. What is the lesson?

At the time of Google’s IPO, investors didn’t know about gmail, Youtube, Android and countless other cloud services, innovations and venture investments that Google was going to make. Most likely, Google’s management also had no idea that it will purchase and develop those services.

Some might make the valid argument that there’s no lesson at all. You cannot make statistically significant conclusions based on one case of a company that is everything but ordinary. If anything, there is evidence that buying a basket of the most expensive stocks in the market is a poor long-term investment.

And yet, if you study the history of most of the best performing stocks, you will realize that that had three things in common:

1) they spend a lot of time on the 52-week high list.

2) they were considered to be expensive at the beginning stages of their price ascent.

3) They managed to outgrow their high P/E ratios

Having a high P/E is not a guarantee of future success. On the contrary. It is a huge hurdle, because it signifies big expectations that need to be met. Market is forward-looking, but it is not naive. It might have big expectations for certain fast growing, innovative companies, but it also expects those companies to deliver at some point of time.

If you filter out all stocks with high P/E, you would have missed on almost every single winner in the stock market. Truth is that you would have missed on almost every single major loser too, but there is a very simple way to filter out the potential losers – price.