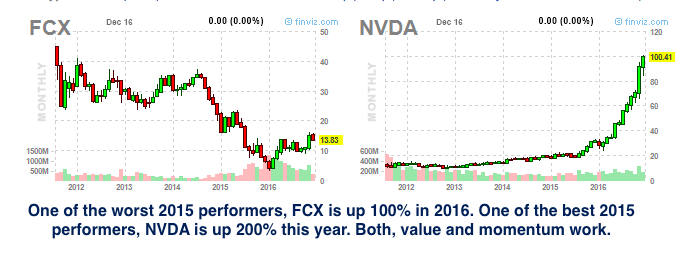

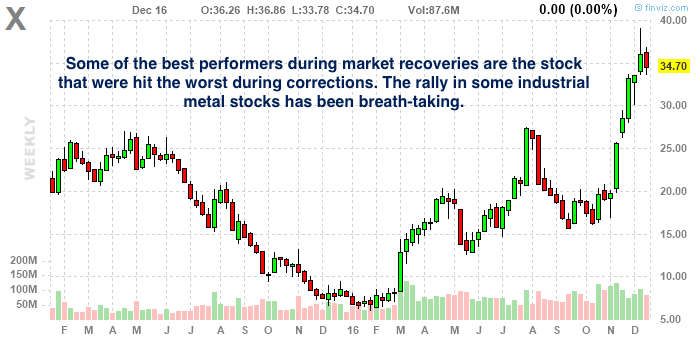

137 stocks more than doubled in 2016 (they are currently priced above $4 and trade over 100k share per day). Many of them belong to sectors that no one expected to see among the big winners in early 2016 – oil & gas and industrial metals. Only four out of the 137, had a good 2015 and can be labeled momentum stocks. All others are mean-reversions in beaten-down stocks. This distribution is unique for 2016. There was a major correction at the end of 2015 and the beginning of 2016 and then a major recovery. Most of the best-performing stocks after deep market corrections are the ones that got hit the worst during the correction. In most years, the best performers are equally distributed between momentum (stocks that had a great previous year) and mean-reversion (stocks that had a horrible previous year).

Basic materials: 59

Consumer goods: 7

Financial: 7

Healthcare (including biotech): 13

Industrial goods: 14

Services: 14 (mostly airlines, education svs, shipping)

Technology: 19 (mostly semiconductors like AMD and NVDA)

Utilities: 4

Here are the top 15 in term of performance:

Check out my newest book: Top 10 Trading Setups – How to find them, When to trade them, How to make money with them