Fred Wilson is a seasoned venture capitalist with one of the best track records in the industry. He started Union Square Ventures in 2005 by raising $125 million for early stage investments in Internet companies. By 2017, he has managed to distribute $1.6 billion to his investors and he is not done. Fred recently gave a speech at MIT. Here are a few quotes that stand out for me:

On working with entrepreneurs:

Working with entrepreneurs is a challenging endeavor. It is also an incredibly rewarding endeavor. I think of it as parenting or teaching a very willful and talented child. It is not for the faint of heart but if you do it well, if you do it right, you can have a tremendous impact on both the entrepreneur and the world. It is these dreamers, these hackers, these unsatisfied souls who end up making things and companies that push us forward and change our lives, mostly for the better.

On early stage investing:

Seeds and early series A investments are the way that you can make a hundred times your money in the venture business. I am not aware of another legal means to do that.

Enthusiasm and appreciation are crucial in VC investing:

A VC’s most important role is that of a cheerleader. I know that seems like nothing. How hard is it to be a cheerleader? But it is everything. And very few VCs do it.

You need a cheerleader in your life:

Joanne is the secret to my success. She understood that being supportive was important. She believed in me from day one. She pushed me and she knew who I can be before I did.

Good judgment comes from experience and experience often comes from bad judgment.

F*cking up royally is good for you if you take the time to learn from it. I am who I am because of Flatiron. This is where my belief system comes from, my instincts and my insights.

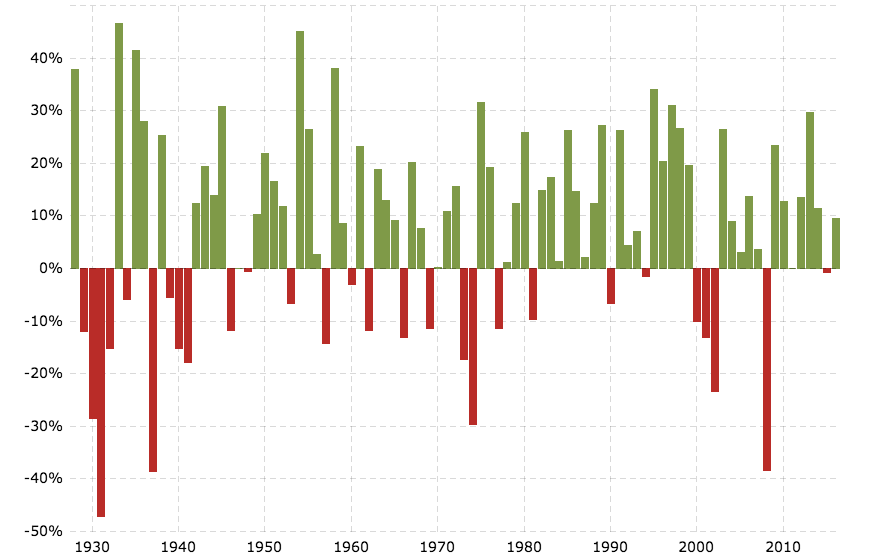

The best time to invest:

The best time to invest in something is when nobody believes in it besides you. You have to totally believe in it and you have to know why.

The entrepreneurs are VC’s customers:

The entrepreneurs are VC’s customers. This is something I learned for myself. I grew up in the business and it was always: “Our customers are our investors. We got to make our investors happy. We have to do a nice annual meeting. We have to write a nice letter”. This was something that resonated in the culture of Euclid Partners (his first VC firm). That’s wrong. Our customers are the entrepreneurs and the companies that they build. Our investors are our shareholders.

VCs are service providers to entrepreneurs. We ride on their coattails. Even though venture capital requires a sophisticated understanding of finance, markets, technology, markets, strategy, it is ultimately a people business. And learning how to be a successful VC is learning how to work with people. A particular breed of people, who are at the same time charismatic, brilliant, frustrated, anxious, and fragile. And our job is to meet them right there where they are and support them with all our might.

What is he looking for in an entrepreneur?

1. Charisma – entrepreneurs have to be able to convince people to suspend disbelief. They have to convince investors, people to join their team, customers, the skeptical world at large. It’s not salesmanship. It is something more than that. I really think of it as charisma. That is necessary but not sufficient.

2.Technical expertise – knowing how to make something, not outsourcing the making to somebody else is really important. It doesn’t mean that you have to build it, but you need to be technical enough to understand what is involved in the making of it.

3. Integrity – is this person going to be honest, is he going to be a good partner, can we work together?

What does it take to be a great angel investor

1.Build a broad-based portfolio. Lot’s of investments because most of them are not going to work out. You need a lot of diversification. More than a typical venture firm will need.

2. Build networks with other angel investors. The more other angel investors you know, the better because you want to syndicate your investments with other people. You want to have many people you can call to try to get in into the deals that you want to do.

3. You will have to help the entrepreneur to get to VC firms. I watch my wife do this all the time. She is tireless in helping the founder she works with to get their series A or even series B round because she knows that her investment is not going to work if she can’t get the follow-up capital.

How to get into the venture business

The conventional wisdom and the advice I often give are “go work in a bunch of startups”. Spend your 20s and 30s working in startups and then, spend your 40s, 50s, and 60s working in venture capital. This is generally a good advice. Most of the people I know who have done that are very good, but this is not the path I took. So, it is a little disingenuous for me to say that. Actually, none of the very best VCs from my generation took that path.